VUL Optimizer® Max

For policyholders who are ready to live life to the max, VUL Optimizer® Max provides a tax-free retirement income strategy and provides a prepackaged variable universal life (VUL) strategy that:

- Dramatically simplifies and shortens the entire associated process and experience to 48 hours, from beginning to end.

- Doesn't require labs, exams or attending physicians statement (APS).

- Provides a death benefit and allows flexible access to potentially tax-free income through policy loans and withdrawals1, and tax-deferred growth.

So your policyholders can help maximize their time in retirement!

Resources to use and share

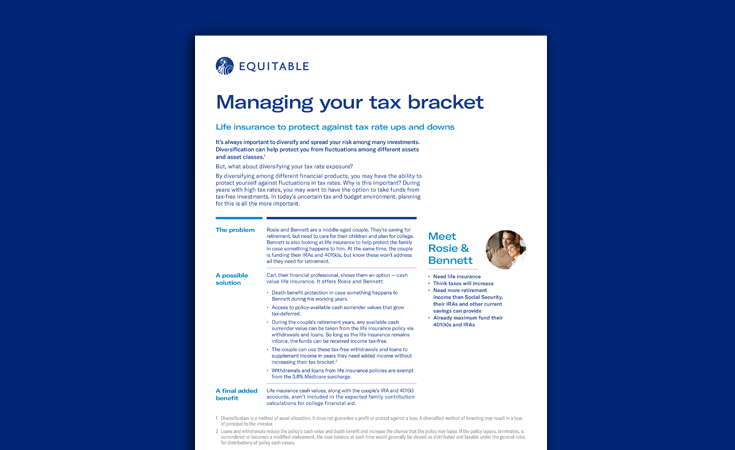

Tax-Efficient Retirement Income

Discover the benefits of using a 7702 cash value life insurance to manage tax brackets in retirement

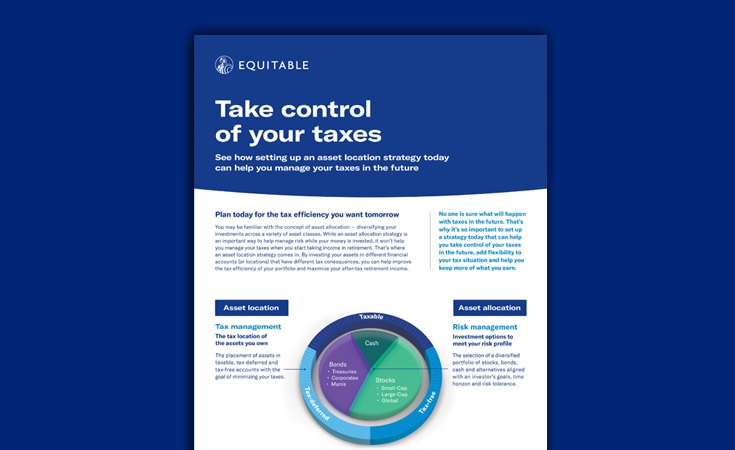

Asset Location Client Brochure

Help clients understand about the placement of assets in taxable, tax-deferred and tax-free accounts with the goal of minimizing taxes

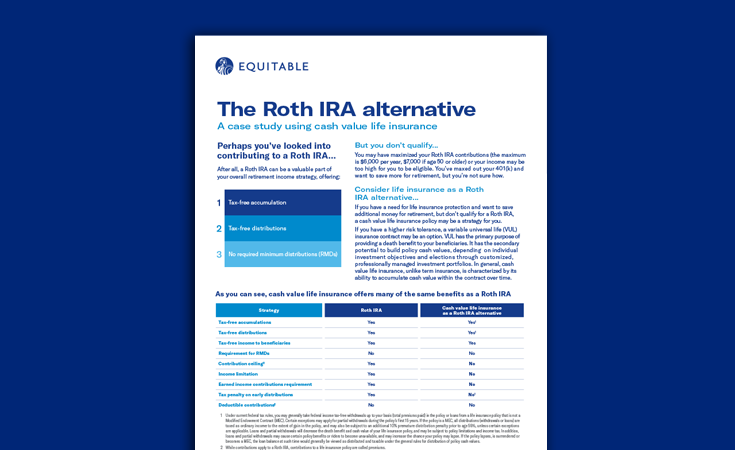

Roth IRA Alternative

See how cash value life insurance has many of the same benefits as a Roth IRA

Why choose VUL Optimizer® Max?

VUL Optimizer® has investment risk including the possible loss of principal invested.

A variable universal life insurance contract is a contract with the primary purpose of providing a death benefit. It is also a long term financial investment that can also allow potential accumulation of assets through customized, professionally managed investment portfolios. These portfolios are closely managed in order to satisfy stated investment objectives. There are fees and charges associated with variable life insurance contracts including mortality and risk charges, administrative fees, investment management fees, surrender charges and charges for optional riders.

Client materials

-

Documents to view or email to clients

- Asset Location Client Brochure

- VUL Optimizer® Max Client Flyer

- VUL Optimizer® Max client presentation

- Managing Your Tax Bracket ($100K)

- Managing Your Tax Bracket ($350K)

- Roth IRA Alternative

- Tax-Efficient Retirement Income (7702 tax-wrapper)

- VUL Investment Options Brochure

- VUL Investment Series Flyer

- Asset Characteristics-Tax Facts

- VUL Optimizer® Client Brochure

- VUL Optimizer® Fact Card

Financial Professional materials

For more about VUL Optimizer® Max contact your Equitable representative

1. Under current federal tax rules, your clients generally may take income-tax-free partial withdrawals under a life insurance policy that is not a modified endowment contract (MEC), up to your clients basis in the contract. Additional amounts are includible in income. The IRS places a limit on how much money can go into life insurance premiums for the policy and how quickly such premiums can be paid in order for the policy to retail all of its tax benefits. If certain limits are exceeded, a MEC results. MEC policyholders may be subject to taxes on distributions on an income-first basis, that is, to the extend there is gain in their policies, and penalties, and penalties on any taxable amount if they are not age 59 1/2 or older. Policy loans and withdrawals will reduce the face amount and cash value of the policy. Clients may need to fund higher premiums in later years to keep the policy from lapsing.

2. Tax Alpha is a method by which an investor is able to, throughout his/her life, allocate funds to various asset location wrappers, to better enable them to manage, and ultimately minimize/hedge, their ongoing tax bill in retirement.

The VUL Optimizer® Max is a VUL Optimizer® policy with a standard plus underwriting class. VUL Optimizer® Max allows for potential insureds, ages 20 -55, to qualify for a standard plus underwriting class without labs, exams or an attending physicians statement (APS) when the requested face amount is no greater that $2,000,000 and planned annualized premium requirements are met in the first 5 policy years. Traditional VUL Optimizer® underwriting that may require additional items or information such as labs, exams and an APS is also available which may result in a better or worse underwriting class.

VUL Optimizer® Max is a VUL Optimizer® policy with a standard plus underwriting class and is referred to as VUL Optimizer®. VUL Optimizer® is a flexible premium variable life insurance policy issued in New York and Puerto Rico by Equitable Financial Life Insurance Company (Equitable), New York, NY; and in all other jurisdictions by Equitable Financial Life Insurance Company of America (Equitable America), an Arizona Stock Corporation with its main administrative office in Jersey City, NJ; and is distributed by Equitable Advisors, LLC (member FINRA, SIPC) (Equitable Financial Advisors in MI and TN) and Equitable Distributors, LLC, 1290 Avenue of Americas, New York, NY 10104. Equitable America is not licensed to conduct business in New York and Puerto Rico. When sold by New York state-based (i.e., domiciled) financial professionals, VUL Optimizer® is issued by Equitable Financial Life Insurance Company (New York, NY). Equitable and Equitable America are separate companies, and each insurance company has sole responsibility for its life insurance obligations.

VUL Optimizer® is sold by prospectus only that contains complete information on investment objective, fees charges and expenses. Clients should read the prospectus carefully before investing or sending money. Visit this page for the current prospectus.

For Financial Professional Use Only/Not for Distribution to the Public

This webpage is not a complete description of all the material provisions of the VUL Optimizer® variable life insurance policy. This webpage must be preceded or accompanied by the VUL Optimizer® product prospectus and any applicable prospectus supplements. The prospectuses contain more complete information about the policy, including investment objectives, risks, charges, expenses, limitations and restrictions. Please read the prospectuses and consider the information carefully before purchasing a policy or sending money. The link above will provide you a copy of the current prospectus.