A cross purchase buy-sell for businesses with multiple owners

If your clients’ business is owned by multiple people, but they want the benefits of a cross purchase buy-sell strategy, try a trusteed cross purchase instead.

How does this strategy work?

In a cross purchase buy-sell agreement, each business owner buys a life insurance policy on the other owner(s). With multiple owners, this can get very complex and complicated. Instead, try a trusteed cross purchase buy-sell, in which a third-party (acting as trustee) takes care of the buy-sell arrangement. Each owner transfers his or her share of the business to the trust, then the trustee purchases a single life insurance policy on each owner. The trust is the owner and beneficiary of the policies.

When one of the owners passes away, the life insurance benefit goes to the trustee, who in turn pays the deceased owner’s estate for their business interest. Then the trustee allocates the deceased owner’s shares to the surviving owners so they each have an equal amount.

Benefits of this strategy:

- Fewer policies are needed, compared to a traditional cross purchase buy-sell arrangement.

- The policies and cash values are generally not subject to the business’ creditors.

- The surviving shareholders will receive full basis credit for the purchase of the stock. This will reduce the capital gains tax when the surviving owners eventually sell the business.

- The life insurance proceeds will not trigger Corporate Alternative Minimum Tax (AMT), because the policy is not owned by a C Corporation.

Considerations to keep in mind:

- The owners will need to use their own after-tax funds to pay for the life insurance policies, and premiums are not deductible.

- If the owners are different ages or would be rated differently, one may have to pay a disproportionate amount of premiums.

- The company cannot record the cash value in the policy as a business asset.

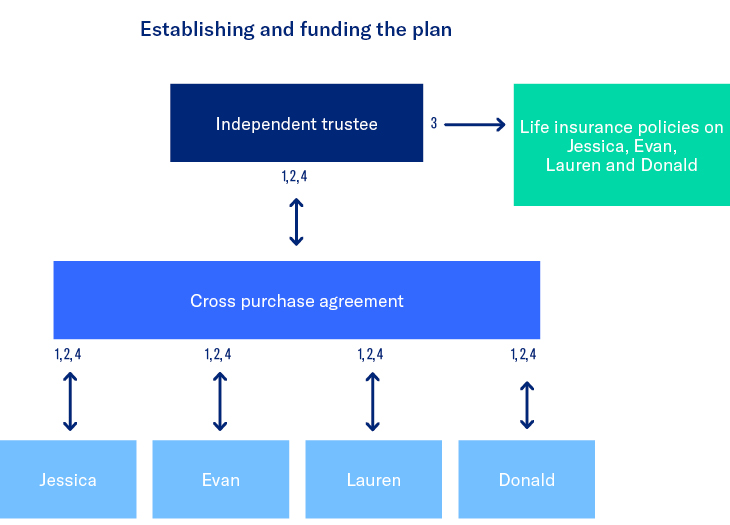

Strategy in action - establishing and funding the plan

- Jessica, Evan, Lauren and Donald own a flower shop called Fancy Flowers. Here’s how the strategy would work.

1. Jessica, Evan, Lauren and Donald each sign a cross purchase agreement with an independent trustee.

2. Each endorses their stock certificates in blank and delivers them to the trustee.

3. Each agrees to allow the trustee to take out an insurance policy on his or her life.

4. Each periodically contributes funds to allow the trustee to pay the premiums on the policies

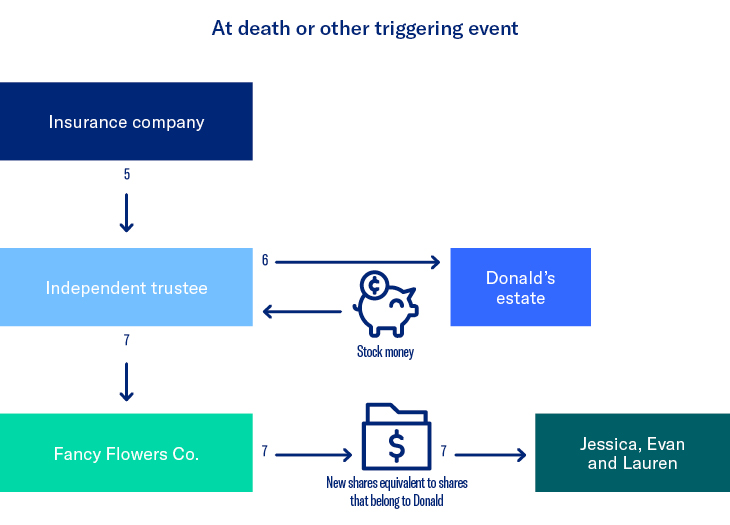

Strategy in action - a triggering event

5. Assuming Donald dies, the insurance company pays the death benefit to the trustee.

6. The trustee pays Donald's estate in exchange for his business interest.

7. The trustee then sees that the Fancy Flowers Company issues new shares to the surviving owners (Jessica, Evan and Lauren), equal to the shares that belonged to Donald.

Prospective client

- Business with 3 or more owners

- Wants to ensure that the business will continue with the surviving owners if one owner passes away

- Worried about paying corporate Alternative Minimum Tax (AMT)

- Wants to keep extra cash value off the books and not subject to the creditors of the business

Highlighted product(s) with this concept

BrightLife® Grow

VUL Optimizersm

Financial Professional materials

-

Marketing materials

Please be advised that this material is not intended as legal or tax advice. Accordingly, any tax information provided in this material is not intended or written to be used, and cannot be used, by any taxpayer for the purpose or avoiding penalties that may be imposed on the taxpayer. The tax information was written to support the promotion or marketing of the transaction(s) or matter(s) addressed and your clients should seek advice based on their particular circumstances from their own tax and legal advisors.

Life insurance products are issued by Equitable Financial Life Insurance Company (New York, NY) or Equitable Financial Life Insurance Company of America (Equitable America), an Arizona stock corporation with its main administration office in Jersey City, NY and are co-distributed by Equitable Network, LLC (Equitable Network Insurance Agency of California in CA; Equitable Network Insurance Agency of Utah in UT; Equitable Network of Puerto Rico, Inc. in PR), and Equitable Distributors, LLC. Variable Products are co-distributed by Equitable Advisors, LLC (Member FINRA, SIPC) (Equitable Financial Advisors in MI and TN) and Equitable Distributors, LLC. Equitable, Equitable America, Equitable Advisors, Equitable Network, LLC and Equitable Distributors do not provide tax or legal advice.