Keep key executives with a BATL Plan®

Highly paid executives often struggle to find ways to save enough for retirement. You can help your business clients attract and retain key employees by offering a BATL Plan.®

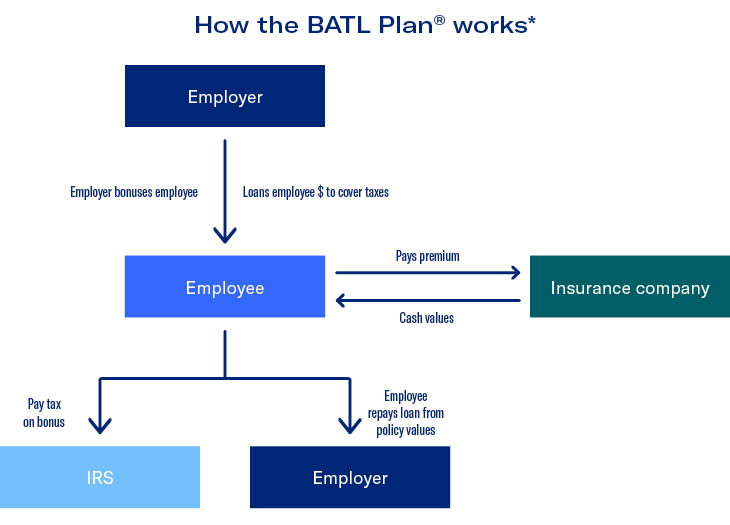

How does this strategy work?

Similar to an Executive Bonus arrangement, a Bonus and Tax Loan (BATL) Plan® allows your business owner clients to choose the key executives they want to reward and retain. Through a BATL Plan,® the employee purchases a cash value life insurance policy and pays the premiums with the bonus he or she receives from the employer. While the bonus itself is subject to income tax, the employee doesn’t pay it from his own assets. Instead, he or she receives a loan from the employer to cover the tax bill and is charged interest on that loan based upon the current Applicable Federal Rate. This loan interest can be paid each year out of pocket or accrued with the outstanding loan. As a result, the full amount of the bonus is used to pay premiums on the policy, maximizing its cash value accumulation potential. Once the employee retires, he or she can take withdrawals from the cash value to pay for retirement expenses and to repay the employer the outstanding loan as well as any interest due, if accrued.

Here’s an example of the BATL Plan® in action

- Mr. Jones is an executive, non-smoker, in good health.

- He’s highly compensated and in the 35% marginal income tax bracket.

- He is concerned about the adequacy of his retirement savings and knows he can’t save all he would like in the company’s 401(k) plan.

- Each year, he receives a bonus, which would result in additional income taxes.

- In a typical bonus arrangement, Mr. Jones would need to come up with that extra money or use part of his bonus to pay the taxes. Instead, he takes a loan from his employer for the amount of the tax and is able to put the whole bonus amount into a permanent life insurance policy.

- His employer charges him interest on the loans, based upon the current Applicable Federal Rate, which may accrue over the years.

- At retirement, he is able to take an annual withdrawal from his policy’s cash value for 15 years, a portion of which goes to pay back his employer for the loans and interest.

Not only does the BATL Plan® help Mr. Jones bridge his retirement income shortfall, but it doesn’t cost his employer that much after taxes.

Prospective client

- Non-public company with highly compensated executives or key employees with 10 or more years before retirement and a need for life insurance.

- Key employees should already be deferring the maximum allowed to their other retirement accounts and have a need to supplement their retirement income.

Highlighted product(s) with this concept

BrightLife® Grow

VUL OptimizerSM

Client materials

-

Documents to view or email to clients

Financial Professional materials

-

Marketing materials

Under current federal tax rules, clients generally may take federal income tax-free withdrawals up to their basis (total premiums paid) in the policy or loans from a life insurance policy that is not a Modified Endowment Contract (MEC). Certain exceptions may apply for partial withdrawals during the policy’s first 15 years. If the policy is an MEC, all distributions (withdrawals or loans) are taxed as ordinary income to the extent of gain in the policy, and may also be subject to an additional 10% premature distribution penalty prior to age 59½, unless certain exceptions are applicable. Loans and partial withdrawals will decrease the death benefit and cash value of the life insurance policy and may be subject to policy limitations and income tax. In addition, loans and partial withdrawals may cause certain policy benefits or riders to become unavailable and may increase the chance the policy may lapse. If the policy lapses, is surrendered, or becomes an MEC, the loan balance at such time would generally be viewed as distributed and taxable under the general rules for distribution of policy cash values.

Please be advised that this webpage is not intended as legal or tax advice. Accordingly, any tax information provided is not intended or written to be used, and cannot be used, by any taxpayer for the purpose of avoiding penalties that may be imposed on the taxpayer. The tax information was written to support the promotion or marketing of the transaction(s) or matter(s) addressed, and clients should seek advice based on their particular circumstances from an independent tax advisor. Neither Equitable nor its affiliates provide legal or tax advice.

Life insurance products are issued by Equitable Financial Life Insurance Company (New York, NY) or Equitable Financial Life Insurance Company of America, an Arizona stock corporation with its main administration office in Jersey City, NJ 07310 and are co-distributed by Equitable Network, LLC (Equitable Network Insurance Agency of California in CA; Equitable Network Insurance Agency of Utah in UT; Equitable Network of Puerto Rico, Inc. in PR), and Equitable Distributors, LLC. Variable products are co-distributed by Equitable Advisors, LLC (Member FINRA, SIPC) (Equitable Financial Advisors in MI and TN) and Equitable Distributors, LLC. When sold by New York based (i.e. domiciled) financial professionals life insurance products are issued by Equitable Financial Life Insurance Company, (NY, NY).