Using life insurance to help minimize taxes in retirement

If your clients expect to be in a high tax bracket in retirement or are worried about taxes rising, they can use cash value life insurance to help supplement their retirement income.

How does this strategy work?

Instead of drawing income from investments that are fully or partially taxed during retirement, your clients can help keep their tax bracket down by integrating distributions from cash value life insurance into the mix. By purchasing life insurance, your clients can protect their families and potentially build policy cash values. At retirement, they can take tax-free loans or withdrawals from the cash value to supplement their retirement income, thus helping to minimize their taxes.

Strategy in action

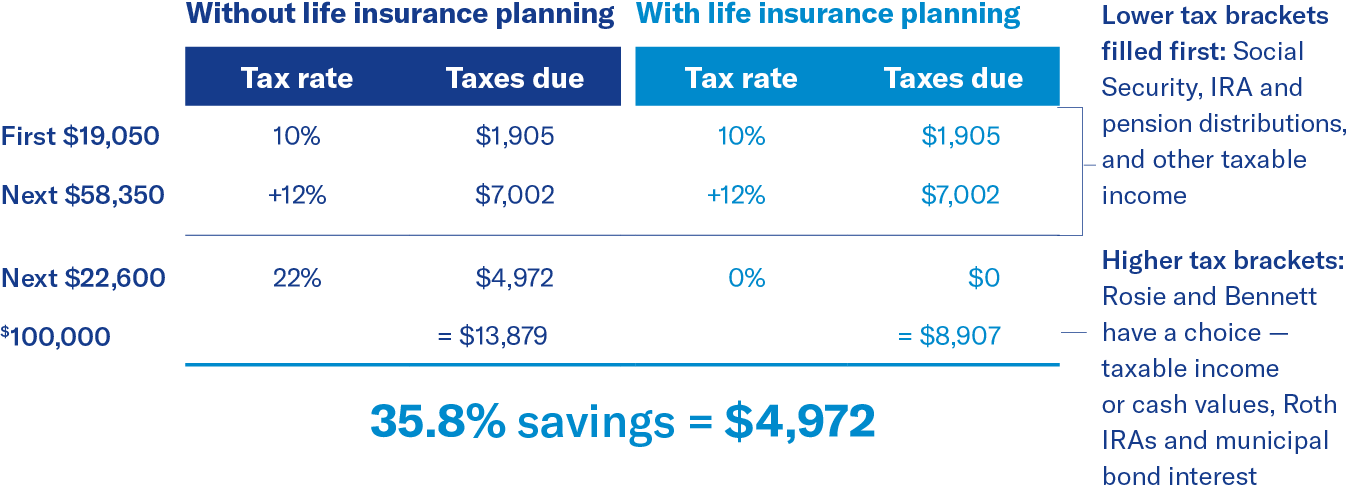

- Bennett and Rosie need life insurance to protect their family.

- They’ve maxed out their qualified retirement plans and want to save more money for the future.

- They’re worried that once they retire, their income will push them into a higher tax bracket than they want.

- They estimate they’ll need $100,000 per year in retirement.

- Bennett purchases a cash value life insurance policy at age 45.

- When they retire, they take non-discretionary income from Social Security and required distributions from their taxable retirement funds. This fills up their lower tax brackets.

- As they approach the higher tax brackets, they can minimize taxes by accessing life insurance cash values potentially tax free.

Here's how Bennett and Rosie meet their $100,000 target retirement income.

Based on a 45-year-old male, preferred underwriting status, a BrightLife® Grow Indexed Universal Life contract with a death benefit of $500,000 and an annual premium of $10,031 would generate 20 years of income of $25,100 starting at age 66. (Policy uses a current rate of 5.79%. At the guarantee rate the policy lapses in year 24.) Assumes tax calculations made in 2017, filing jointly.

Prospective client

- Needs financial protection for family or business

- Has maximized contributions to qualified plans such as a 401(k)

- Worries about tax rates increasing or being pushed into a higher tax bracket than they want in retirement

- Needs more retirement income than Social Security, their qualified plans, and other current savings can provide

Highlighted product(s) with this concept

BrightLife® Grow

VUL Survivorship

Client materials

-

Documents to view or email to clients

Under current federal tax rules, clients generally may take federal income-tax-free withdrawals up to their basis (total premiums paid) in the policy or loans from a life insurance policy that is not a Modified Endowment Contract (MEC). Certain exceptions may apply for partial withdrawals during the policy’s first 15 years. If the policy is an MEC, all distributions (withdrawals or loans) are taxed as ordinary income to the extent of gain in the policy, and may also be subject to an additional 10% premature distribution penalty prior to age 59½, unless certain exceptions are applicable. Loans and partial withdrawals will decrease the death benefits and cash value of the life insurance policy and may be subject to policy limitations and income tax. In addition, loans and partial withdrawals may cause certain policy benefits and riders to become unavailable and may increase the chance the policy may lapse. If the policy lapses, is surrendered, or becomes an MEC, the loan balance at the time would generally be viewed as distributed and taxable under the general rules for distribution of policy cash values.

Please be advised that this webpage is not intended as legal or tax advice. Accordingly, any tax information provided in this article is not intended or written to be used, and cannot be used, by any taxpayer for the purpose of avoiding penalties that may be imposed on the taxpayer. The tax information was written to support the promotion or marketing of the transaction(s) or matter(s) addressed, and your clients should seek advice based on their particular circumstances from an independent tax advisor. Neither Equitable nor its affiliates provide legal or tax advice.

When sold by New York State-based (i.e., domiciled) Financial Professionals, BrightLife® Grow is issued by Equitable Financial Life Insurance Company (New York, NY).