The 3-bucket approach to protecting a legacy (“Legacy Protect”)

If your clients want to ensure a legacy for their family, have money for retirement and for other financial contingencies, try using this 3-bucket approach.

How does this strategy work?

The first step in the “Legacy Protect” strategy is to segregate your clients’ assets into three distinct buckets:

- Bucket A: The Retirement Fund – Even if your clients want to leave as much as possible for their family, it’s important they have enough for retirement too.

- Bucket B: The Contingency Fund – This includes assets your clients don’t plan to use during their lifetime, but want to keep accessible in case they experience an unexpected financial or medical set-back. For many clients, permanent cash value life insurance, with a long-term care rider, will serve nicely.

- Bucket C: The Legacy Fund – This bucket includes the assets your clients want to leave their heirs. While they may want to maximize the amount they leave their family, many clients invest this bucket too conservatively.

By allocating a portion of the cash flow from Bucket C assets into life insurance, they can diversify the risk of this important segment of their investment. In many cases, it takes as little as 1%, or 100 basis points, from the return on Bucket C assets to purchase a permanent life insurance policy.

Why use life insurance?

- Protects the legacy bucket against unexpected fluctuations in market value leaving your clients’ families with a reduced legacy

- Assures your clients that they can leave an inheritance

- Diversifies their assets, which can also help protect their legacy bucket assets

- Allows your clients to implement broader investment strategies with the remaining assets in the legacy bucket by diversifying the portfolio

- Can potentially provide additional assets for retirement or contingencies through policy cash values

Strategy in action

- Marjorie is 55 years old and is 10-15 years from retirement.

- She has $4 million in investment assets, a 401(k) plan and a “cash balance” pension plan through her employer.

- She wants to make sure she has money for retirement, unexpected financial challenges and can leave a legacy for her children and new grandson.

- Her financial professional recommends the “Legacy Protect” strategy.

Bucket A: Retirement Funds

- $1 million of her investment assets

- Her employer-sponsored retirement plans

- Social Security

Bucket B: Contingency Funds

- $1 million of her investment assets

- She purchases a $500,000 BrightLife® Grow indexed universal life policy with the Long-Term Care ServicesSM Rider, to help protect against unforeseen retirement expenses, including potential long-term care costs.

Bucket C: Legacy Funds

- $2 million of her investment assets

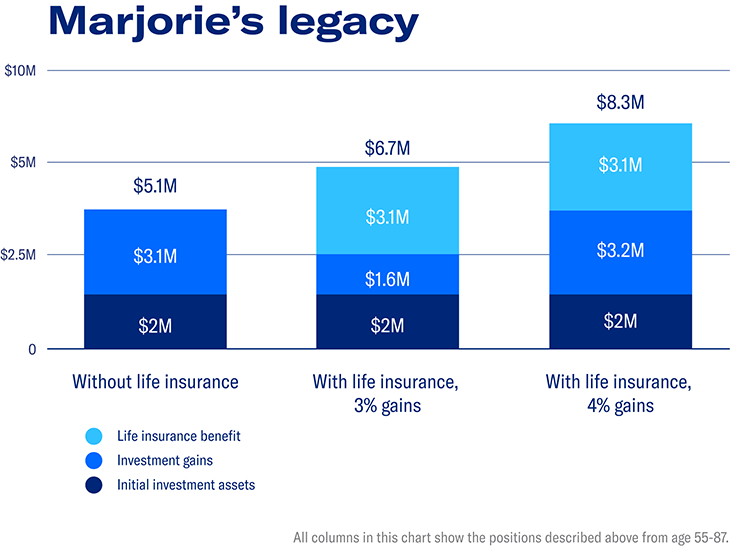

- If she lives until age 87 and earns an average return of 3% (net of taxes) on these assets – her Bucket C assets will have grown to over $5.1 million.

What if Marjorie repositioned Bucket C assets to help protect and possibly grow her legacy?

- If she takes half of her expected return ($28,217 each year, initially 1.41% or 141 basis points) and purchases a IUL Protect indexed universal life policy with a face amount of $3.1 million, her anticipated legacy at age 87 could reach $6.7 million.

- If her investment advisor thinks that life insurance adds diversification and protection to her portfolio, her advisor may change her investment strategy slightly, by investing a bit more aggressively. If this results in her earning an average return of 4%, her anticipated legacy at age 87 could reach $8.3 million.

Prospective client

- 45-60 year old with 10-15 years until retirement

- Wants to leave a legacy for children and/or grandchildren, but also wants to make sure they have enough money for retirement and other unexpected expenses

- Is healthy and can buy life insurance at a reasonable price

Considerations

Cash value life insurance has many other considerations your clients should review carefully before selecting a policy. Please keep these important points in mind:

- If clients do not keep paying the premium on a life insurance policy, they will lose substantial cash value in early years.

- To be effective, clients need to hold the policy until death. A life insurance policy generally takes years to build up a substantial cash value.

- Tax-free distributions will reduce the cash value and face amount of the policy, and clients may need to pay higher premiums in later years to keep the policy from lapsing.

- Clients must qualify medically and financially for life insurance and for the Long-Term Care ServicesSM Rider.

- Generally, there are many additional charges associated with a life insurance policy including but not limited to a front-end load monthly administrative charge, monthly segment charge, cost of insurance charge, additional benefit rider costs, and surrender charges.

Highlighted product(s) with this concept

VUL Optimizersm

Client materials

-

Documents to view or email to clients

Financial professional materials

-

Marketing materials

The Long-Term Care ServicesSM Rider is available for an additional fee and does have restrictions and limitations. A client may qualify for the life insurance but not the rider.

Please be advised that this webpage is not intended as legal or tax advice. Accordingly, any tax information provided is not intended or written to be used, and cannot be used, by any taxpayer for the purpose of avoiding penalties that may be imposed on the taxpayer. The tax information was written to support the promotion or marketing of the transaction(s) or matter(s) addressed, and clients should seek advice based on their particular circumstances from an independent tax advisor. Neither Equitable nor its affiliates provide legal or tax advice.

Life insurance products are issued by Equitable Financial Life Insurance Company (New York, NY) or Equitable Financial Life Insurance Company of America (Equitable America), an Arizona stock corporation with its main administration office in Jersey City, NY and are co-distributed by Equitable Network, LLC (Equitable Network Insurance Agency of California in CA; Equitable Network Insurance Agency of Utah in UT; Equitable Network of Puerto Rico, Inc. in PR), and Equitable Distributors, LLC. Variable Products are co-distributed by Equitable Advisors, LLC (Member FINRA, SIPC) (Equitable Financial Advisors in MI and TN) and Equitable Distributors, LLC.