Premium financing for high-net worth clients

If you have clients with a net worth of $5 million or more who need life insurance protection, they may be able to finance the premiums so as not to disrupt their other appreciating assets.

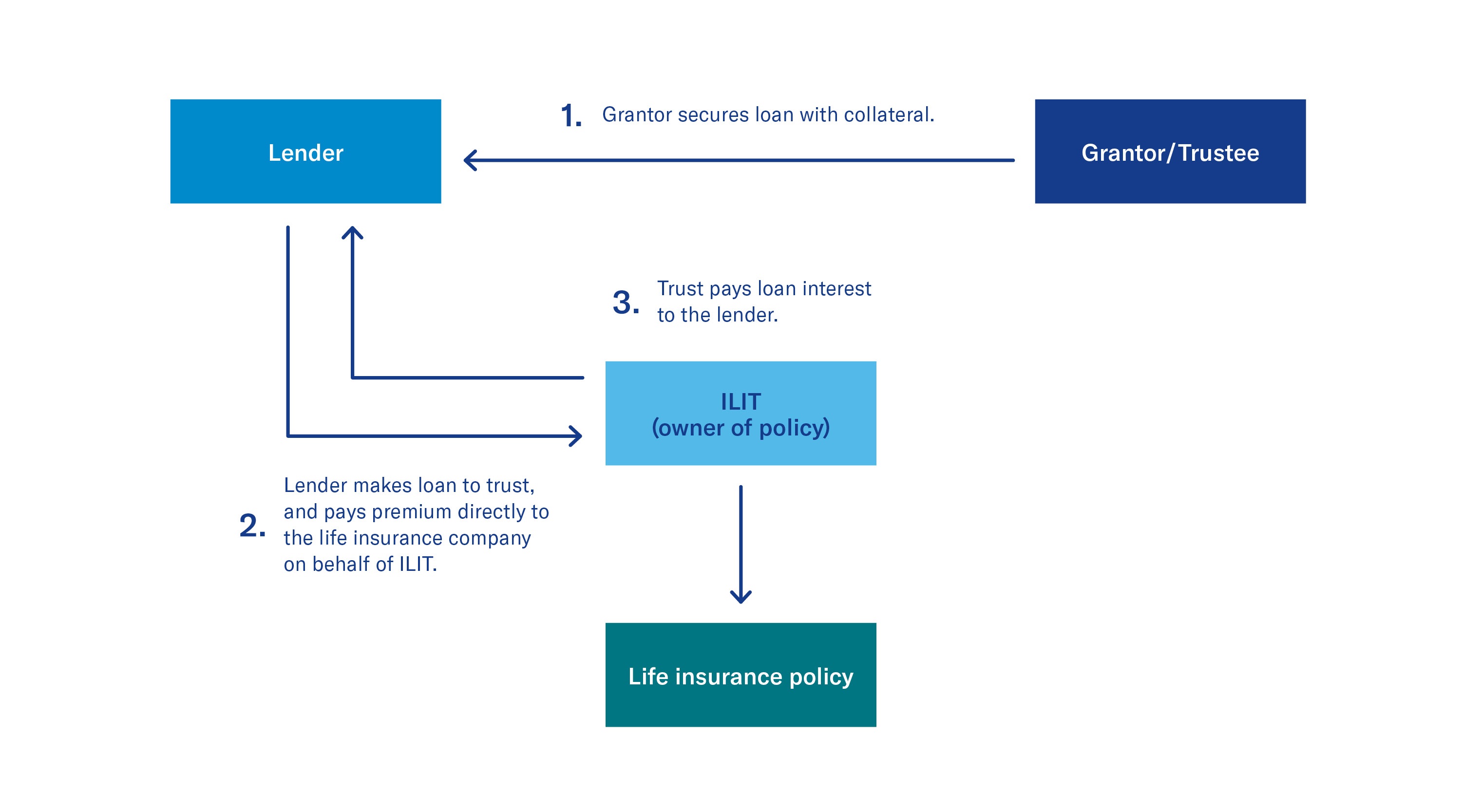

How does this strategy work?

Instead of liquidating their assets to pay life insurance policy premiums, high-net worth clients may be able to secure loans from a third-party lender to pay the premiums. This strategy can work if the interest on the loans is less than the appreciation your clients anticipate earning on their other assets, and the policy is owned by an Irrevocable Life Insurance Trust (ILIT). Loan interest is paid annually and the loan principal can typically be repaid at any time up to and including at the clients’ death. If there is a loan balance at the clients’ death, part of the life insurance death benefit would repay the loan and the remainder would go to the clients’ beneficiaries.

In the right circumstances, financing life insurance policy premiums may provide a client with a better internal rate of return than paying premiums out of pocket. This will vary greatly based on the clients’ loan terms, how the non-liquidated assets perform, and the point at which the loan is repaid.

Strategy in action

Borrowing funds to pay insurance premiums may only be completed with a properly licensed lending institution. Neither Equitable, Equitable America, or its agents are licensed by any state to act as a lender. The life insurance purchase and the loan are separate and distinct transactions conducted by separate entities. A person may qualify for the loan but not the insurance, and vice versa.

Prospective client

- Has a net worth of $5 million or more, with significant collateral to obtain loans

- Has a need for life insurance protection

- Wishes to pass on assets to beneficiaries

- Has illiquid or appreciating assets

Highlighted product(s) with this concept

BrightLife® Grow

Client materials

-

Documents to view or email to clients

Financial Professional materials

-

Marketing materials

Please be advised that this webpage is not intended as legal or tax advice. Accordingly, any tax information provided in this article is not intended or written to be used, and cannot be used, by any taxpayer for the purpose of avoiding penalties that may be imposed on the taxpayer. The tax information was written to support the promotion or marketing of the transaction(s) or matter(s) addressed, and your clients should seek advice based on their particular circumstances from an independent tax advisor. Neither Equitable nor its affiliates provide legal or tax advice.

Life insurance products are issued by Equitable Financial Life Insurance Company, Equitable Financial (New York, NY) or Equitable Financial Life Insurance Company of America (Equitable America), an Arizona stock corporation with its main administration office in Jersey City, NJ and are co-distributed by Equitable Network, LLC (Equitable Network Insurance Agency of California in CA; Equitable Network Insurance Agency of Utah in UT; Equitable Network of Puerto Rico, Inc. in PR), and Equitable Distributors, LLC. Variable Products are co-distributed by Equitable Advisors, LLC (Member FINRA, SIPC) (Equitable Financial Advisors in MI and TN) and Equitable Distributors, LLC.