Too much of one stock?

If your clients are looking to transfer wealth and have a high concentration of one stock in their portfolio, they may want to sell some stock (and pay low capital gains taxes) and purchase life insurance.

How does this strategy work?

With capital gains rates at near historic lows, now may be a good time to reposition some of your client’s portfolio. Selling a portion of concentrated stock and using the proceeds to purchase cash value life insurance may be a good alternative to help ensure a certain level of wealth transfer. By moving a portion of the gain from the sale of their stock into life insurance, your clients can:

- Provide an income-tax-free life insurance benefit for their family

- Provide a specific sum of money for wealth transfer, regardless of what happens in the market

- Potentially accumulate tax-deferred cash value

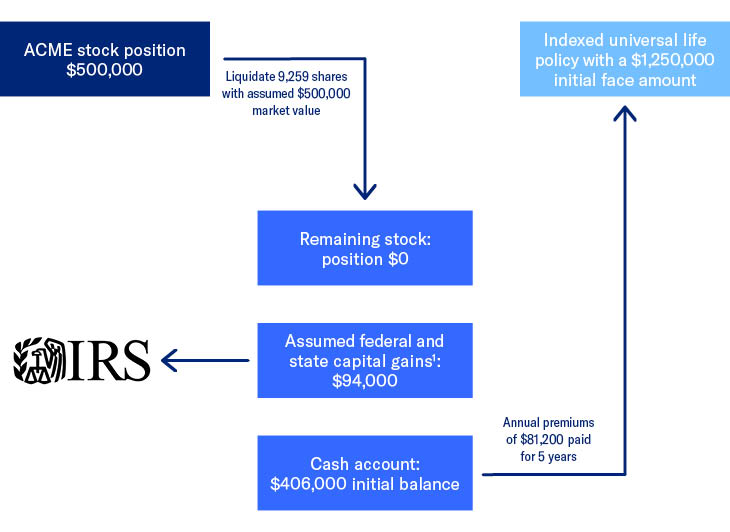

Strategy in action

- Mary and John are 55 years old and on track with their retirement savings.

- Six years ago, they bought stock in Acme, a medical tech company, and its value has skyrocketed to $500,000, representing a quarter of their portfolio.

- They need life insurance and want to diversify their portfolio further.

- They sell their Acme stock for $500,000, pay $94,000 in capital gains and over the next five years, pay premiums of $81,200 into an indexed universal life insurance policy. That will give them a life insurance benefit to pass, income-tax-free, to their family, of $1,250,000 – significantly more than passing the stock itself and with much less risk.

1 Includes 3.8% Medicare Surcharge tax.

The policy premium and death benefit amounts used for this case are intended only to help demonstrate the planning concept discussed and not to promote any specific product. The values are broadly representative of rates that would apply for a policy of this type and size for the insured’s health and the ages noted in the example. To determine how this approach might work for a client, individual illustrations based on their own individual age and underwriting class, containing both guaranteed charges and guaranteed interest rates as well as other important information, should be prepared.

Prospective client

- Has a life insurance need

- 45-65 years old, but may be older

- Net worth of at least $1 million, exclusive of residence

- May be a corporate executive with stock in the company that makes up a large portion of their net worth

- May have a large portion of wealth tied to a stock with family or sentimental value

Financial Professional materials

Please be advised that this webpage is not intended as legal or tax advice. Accordingly, any tax information provided in this guide for producers is not intended or written to be used, and cannot be used, by any taxpayer for the purpose of avoiding penalties that may be imposed on the taxpayer. The tax information was written to support the promotion or marketing of the transaction(s) or matter(s) addressed, and clients should seek advice based on their particular circumstances from an independent tax advisor.

Life insurance products are issued by Equitable Financial Life Insurance Company (New York, NY) or Equitable Financial Life Insurance Company of America, an Arizona stock corporation with its main administration office in Jersey City, NJ 07310 and are co-distributed by Equitable Network, LLC (Equitable Network Insurance Agency of California in CA; Equitable Network Insurance Agency of Utah in UT; Equitable Network of Puerto Rico, Inc. in PR), and Equitable Distributors, LLC. Variable products are co-distributed by Equitable Advisors, LLC (Member FINRA, SIPC)(Equitable Financial Advisors in MI and TN) and Equitable Distributors, LLC. When sold by New York based (i.e. domiciled) financial professionals life insurance products are issued by Equitable Financial Life Insurance Company, (NY, NY).